Which funding model is right for your business?

Most employers pay 350% of the actual cost for medical services — and the big box carriers keep the savings. We designed innovative health plans and a unique strategy to changes that.

Your health plan is designed to be expensive.

The carrier, the hospital, and the Pharmacy Benefit Manager (PBM) all profit from complexity and inflated prices. These big-box insurance conglomerates own every link in the healthcare chain: the doctors, the pharmacies, the data platforms, and even the “middlemen” (Pharmacy Benefit Managers). This is called vertical integration, and it’s a fancy way of saying they’ve rigged the system to keep your money moving in one big, profitable circle.

By controlling the entire ecosystem, these big players can funnel patients toward higher-priced services they own—regardless of whether patients actually get better service and prices elsewhere. That’s the system working exactly as designed — just not for you.

The good news is that you don’t have to play by their rules. A growing movement of forward-thinking business owners is stepping outside the traditional carrier circle. By moving toward level-funding or self-funding models, you break the cycle of inflated prices and gain total transparency over every dollar spent.

A strategy built for your success

You deserve a health plan that rewards efficiency rather than penalizing it. Moving toward a level-funded or self-funded model breaks this cycle by providing total transparency and control over every dollar spent. Instead of paying fixed premiums to a carrier that keeps the surplus when claims are low, these models allow employers to keep the savings and reinvest them into better care.

By utilizing tools like Direct Primary Care, preferred provider networks that charge fair market rates, and transparent pharmacy pricing, companies can actively steer members toward higher-quality and lower-cost care.

Smarter value-based funding for discerning businesses.

When comparing level-funding vs. self-funding for your company’s health plan, you’re evaluating two very different approaches to managing healthcare costs. Each model comes with trade-offs that can significantly affect your budget, cash flow, and administrative responsibilities.

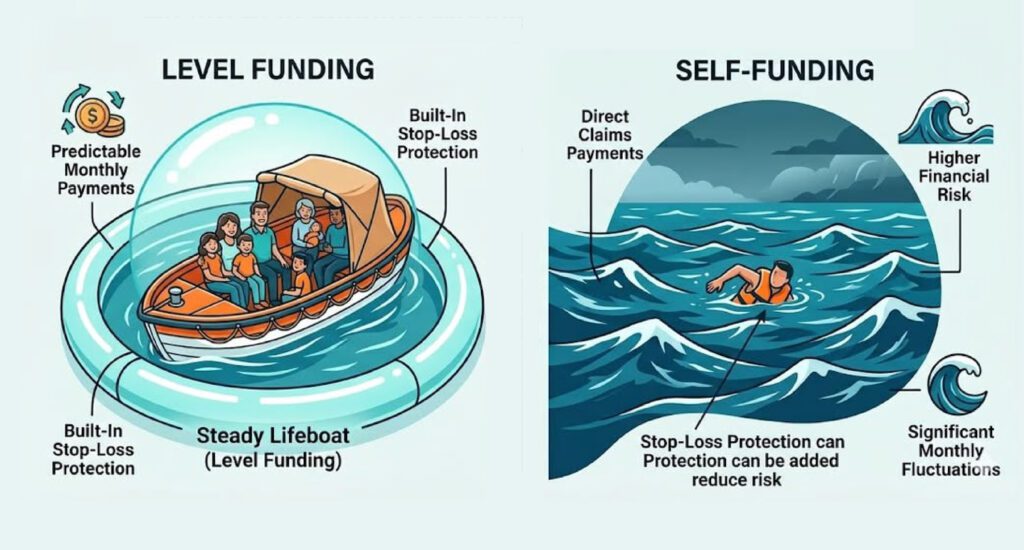

The biggest difference between these two funding models comes down to risk—specifically how much financial risk you’re willing to take on as an employer.

Think of level-funding as being in a life boat while in the financial waters of healthcare costs. You pay the same amount each month, regardless of whether employees submit $100 or $100,000 in claims, and the stop-loss insurance safeguards your company in the event of a high-cost claim event.

Ultimately, choosing between level-funding vs. self-funding isn’t just about numbers—it’s about finding the right balance of predictability, risk, and control for your business.

The pros and cons of level-funding and self-funding

Understanding the advantages and drawbacks of each funding model is essential when choosing between level-funding vs. self-funding.

Both options offer meaningful benefits, but they also introduce different types of financial and administrative considerations.

Level-Funded Plans

Recommended for businesses with fewer than 50.

ADVANTAGES

► Predictable Monthly Costs

One of the biggest benefits of a level-funded plan is budget stability. Your monthly payments are fixed throughout the year, making financial planning easier and eliminating surprise premium spikes.

► Built-In Stop-Loss Protection

Level-funded plans include stop-loss insurance, which protects employers from catastrophic claims. This ensures your financial exposure remains capped, even if one or two employees experience major medical events.

► Improved Cost Transparency

Employers have access to some claims data, which allows them to identify trends and implement programs that encourage healthier behaviors among employees.

► Regulatory Advantages

Because level-funded plans are technically self-funded under ERISA, they are exempt from many state insurance mandates and premium taxes, which can reduce overall plan costs.

POTENTIAL DRAWBACKS

► Renewal Rate Increases

If your employee group experiences high claims in a given year, your renewal rates may increase. These increases can potentially offset previous savings.

► Additional Compliance Requirements

Level-funded plans require employers to handle several additional compliance obligations, including:

- PCORI fee reporting

- ACA reporting requirements

- COBRA administration differences

- Section 105(h) nondiscrimination testing.

► Limited Customization

While more flexible than fully insured plans, level-funded options still lack the full design freedom that comes with self-funded plans.

Self-Funded Plans

Recommended for businesses with more than 50.

ADVANTAGES

► Maximum Plan Design Control

Self-funded plans provide the highest level of customization available. Employers can design their health plans to match their workforce’s specific needs while maintaining control over cost structures.

► Immediate Cost Savings

If claims are lower than expected, the savings remain directly with the employer. There is no waiting period for refunds or credits. Additionally, employers avoid paying the profit margins associated with traditional insurance carriers, which can create significant cost savings.

► Complete Data Transparency

Self-funded plans offer full access to claims data, giving employers deep insight into healthcare spending patterns. This transparency allows companies to develop more effective wellness initiatives, targeted interventions, and cost management strategies.

► Regulatory Consistency

Self-funded plans are governed primarily by ERISA, which means they are largely shielded from varying state insurance regulations. For companies operating in multiple states, this can simplify compliance significantly.

POTENTIAL CHALLENGES

► Higher Financial Risk

Because employers pay claims directly, costs can fluctuate significantly from month to month. If several large claims occur early in the year, the financial impact can be substantial.

► Need for Strong Financial Reserves

Self-funded employers must maintain sufficient financial reserves to cover:

- Unexpected claims spikes

- Incurred-but-not-reported (IBNR) claims

- Potential stop-loss deductibles

Making the right choice for your health plan

Choosing between level-funding vs. self-funding depends largely on your company’s size, workforce characteristics, and financial readiness.

Company Size

For smaller organizations with fewer than 50 employees, level-funding often provides a more comfortable entry point due to its predictable monthly costs.

For larger organizations with 50+ employees, self-funding can become more attractive because risk is spread across a larger employee population, increasing the potential for long-term savings.

Workforce Demographics

The health profile of your workforce plays a major role.

Employers with younger, healthier populations may benefit significantly from self-funding or level-funding compared to fully insured plans.

However, if your workforce includes several employees with ongoing medical needs, the predictability of level-funding may provide greater financial stability.

Financial Readiness and Risk Tolerance

Employers should carefully evaluate their financial position and comfort level with risk.

Self-funding requires:

- Stronger cash reserves

- Greater tolerance for claim volatility

- Strategic claims management

Level-funding can serve as a bridge strategy, allowing employers to gain experience with self-funded mechanics while limiting their financial exposure.

Many organizations begin with level-funded plans before eventually transitioning to full self-funding once they are comfortable with the model.

This approach allows employers to:

- Gain experience with claims funding

- Analyze healthcare utilization patterns

- Develop the internal systems needed for long-term self-funding success

Choosing the right funding strategy for your business

There is no universal answer when choosing between level-funding vs. self-funding. The right solution depends on your company’s workforce size and health, financial readiness, risk tolerance and long-term benefits strategy.

A thoughtful evaluation of these factors—combined with guidance from an experienced benefits advisor—can help you determine the best approach for delivering high-quality healthcare benefits while managing costs effectively.

Whatever option you choose, it’s important not to limit yourself to your current insurance relationships. Take the time to explore all available funding strategies and identify the solution that best supports your business and your employees.

Call 866-549-4199